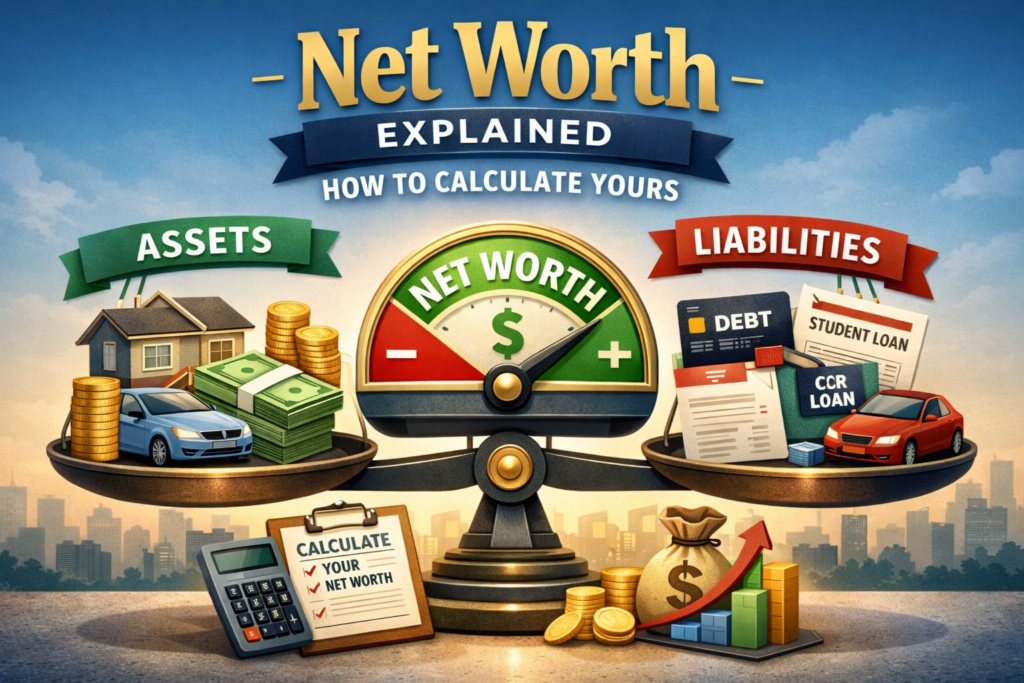

Net Worth Explained: 7 Simple Steps to Calculate Yours Today

Have you ever wondered where you truly stand financially? Not just how much money you earn each month, but the full picture of your wealth, what you own versus what you owe. That single number, your net worth, holds more power than your paycheck, your savings balance, or even your investments. It’s the clearest measure of your financial health, a compass that guides every decision from paying off debt to investing for the future.

Net worth is more than just math, it’s a mirror reflecting your financial habits, your priorities, and the choices that shape your future. While many people focus on income or spending, they often overlook this one figure that tells the full story. Knowing your net worth can reveal opportunities, highlight risks, and even change the way you approach money.

Whether you’re just starting out in your career, building your investment portfolio, or planning for retirement, understanding your net worth is essential. It gives you a realistic view of where you are, so you can plan effectively for where you want to go.

In this post, we’ll unpack what net worth really means, why it matters, and walk you step-by-step through calculating it accurately. By the end, you’ll not only know your number, you’ll know how to use it to grow your wealth, make smarter financial choices, and gain real financial freedom.

What Is Net Worth?

Your net worth is more than just a financial term, it’s a snapshot of your entire financial life. In simple terms, it’s the difference between everything you own (assets) and everything you owe (liabilities). Imagine selling everything you own and paying off all your debts. The amount left over is your net worth.

Assets: are items of value that belong to you. This includes cash, savings, investments, retirement accounts, real estate, vehicles, and personal valuables like jewelry or collectibles. Assets can generate wealth over time, either through appreciation, interest, or income generation.

Liabilities: are obligations you owe to others. They include mortgages, student loans, credit card debt, car loans, and any other borrowed money. Liabilities reduce your net worth because they represent money that must eventually be paid out.

The formula is simple:

Net Worth = Total Assets- Total Liabilities

Your net worth can be positive or negative. A positive net worth means your assets exceed your liabilities, showing that you have built wealth. A negative net worth means you owe more than you own, which is common for students or young professionals just starting their careers. The key is not where you start, but that you track it over time and make steady improvements.

Why Net Worth Matters

Many people overlook net worth because it feels abstract, compared to income or expenses. But understanding it is crucial, and it has real-life consequences for your financial health, planning, and even mental peace. Here’s why it matters:

1. Provides a Complete Financial Picture

Focusing solely on income or monthly savings can be misleading. A high salary doesn’t guarantee wealth if debt levels are equally high. Net worth accounts for both sides, assets and liabilities giving a holistic view of your financial situation. It answers questions like, are you truly building wealth, or just covering expenses?

2. Tracks Progress Over Time

By calculating your net worth regularly, whether monthly, quarterly, or annually you can see whether your strategies are working. Are debts decreasing? Are investments growing? This tracking provides clear feedback on your financial decisions and allows you to make timely adjustments.

3. Aids in Financial Planning

Net worth is a foundation for every major financial goal. Whether you want to buy a home, invest in a business, or plan for retirement, knowing your net worth lets you set realistic targets. Financial advisors often use it as a baseline to recommend investment strategies, debt repayment plans, or asset allocation.

4. Motivates and Holds You Accountable

Seeing a positive trend in your net worth can be incredibly motivating. Conversely, noticing a downward trend highlights areas that need attention. Tracking this number encourages disciplined saving, investing, and debt management, turning financial awareness into action.

Components of Net Worth

To calculate net worth accurately, you need a clear understanding of its two components: assets and liabilities. Breaking them down helps ensure nothing is overlooked.

a) Assets

Assets are everything of value that you own. They can be liquid, investment, or personal property:

1. Liquid Assets:

These are assets that can be converted to cash quickly, often within a few days. Examples include:

Cash in checking or savings accounts

Money market accounts

Short-term investments

Certificates of deposit (CDs)

Liquid assets are crucial because they act as a safety net, allowing you to cover emergencies or unexpected expenses without going into debt.

2. Investment Assets

Investment assets are long-term wealth builders. They include:

Stocks, bonds, mutual funds, ETFs

Retirement accounts like 401(k)s, IRAs, or pensions

Real estate investments (excluding primary residence if used mainly for living)

These assets grow over time and can generate passive income, making them essential for long-term financial security.

3. Personal Property

These are tangible items that hold value but may not necessarily generate income:

Vehicles (cars, motorcycles, boats, RVs)

Jewelry, art, and collectibles

High-value electronics or furniture

While some of these depreciate over time, they still contribute to your overall net worth and should be included for an accurate picture.

b) Liabilities:

Liabilities represent money you owe. They reduce your net worth and can either be short-term or long-term:

1. Short-term Liabilities

These are debts due within a year:

Credit card balances

Personal loans

Unpaid bills or taxes

Short-term liabilities often carry higher interest rates (like credit cards), which makes repaying them quickly a priority for increasing net worth.

2. Long-term Liabilities

These debts have longer repayment horizons, typically over several years:

Student loans

Car loans

Business loans

Long-term liabilities are often manageable if strategically planned, but they still reduce your net worth until paid off.

Some people also include future financial obligations, like taxes owed or legal settlements, though most personal net worth calculations focus on actual, current debts.

Tracking each component carefully ensures your net worth calculation is accurate, actionable, and insightful. It’s not just about numbers, it’s about understanding your financial position so you can make smarter decisions, reduce risk, and grow wealth over time.

Step-by-Step Guide to Calculating Your Net Worth

Now that you understand what assets and liabilities are, the next step is putting the pieces together to calculate your net worth. This process may seem daunting at first, but breaking it into clear steps makes it manageable and even empowering.

Step 1: List All Your Assets

Start by identifying everything you own that has value. Be thorough, and don’t forget items that might seem minor but still contribute to your total net worth.

Categories to include:

Cash & Bank Accounts: Checking, savings, and any cash you have on hand.

Investments: Stocks, bonds, mutual funds, ETFs, and retirement accounts such as IRAs or 401(k)s.

Real Estate: Your home, rental properties, or other land holdings. Always use current market value, not purchase price. Online property valuation tools or recent appraisals can help.

Vehicles: Cars, motorcycles, boats, RVs, or any other transport assets.

Other Valuable Items: Jewelry, collectibles, electronics, or artwork that hold significant value.

Remember, the goal is to capture realistic market value, not sentimental or purchase value. This ensures an accurate reflection of your financial standing.

Step 2: List All Your Liabilities

Next, gather all debts and obligations. This is the part that often gets overlooked but is critical for an accurate calculation.

Include all types of debt:

Credit Card Balances: High-interest debt can drastically affect your net worth.

Loans: Student loans, car loans, personal loans, or business loans.

Mortgage: Include the remaining principal balance, not the total paid over time.

Other Debts: Taxes owed, unpaid bills, or any other financial obligations.

Be thorough, leaving out even small debts can distort your true financial picture.

Step 3: Subtract Liabilities from Assets

Once you have totals for assets and liabilities, the calculation is simple:

Net Worth = Total Assets – Total Liabilities

Positive Net Worth: You own more than you owe, a solid foundation for growth.

Negative Net Worth: You owe more than you own. This is common for young professionals or those with student loans. A negative net worth isn’t failure, it’s a starting point for planning improvements.

Step 4: Analyze Your Net Worth

Calculating your net worth is only the first step. The real value comes from analyzing it:

Track Over Time: Compare monthly, quarterly, or yearly to see trends. Are you moving in the right direction?

Evaluate Asset Allocation: Are your assets concentrated in illiquid forms like real estate, or do you have enough cash and investments to handle emergencies?

Identify Debt Patterns: Is high-interest debt dragging you down? Recognizing these patterns helps you focus on areas that will accelerate growth.

Tips to Improve Your Net Worth

Building net worth isn’t just about earning more, it’s about smartly managing your money. Here are actionable strategies:

Pay Down High-Interest Debt

Debt like credit cards or payday loans can erode wealth faster than anything else. Focus on eliminating these first.Build an Emergency Fund

Save 3-6 months of living expenses in liquid cash. This protects you from financial shocks and prevents new debt.Invest Consistently

Diversified investments in stocks, bonds, or real estate allow your money to grow faster than inflation. Over time, compounding makes a huge difference in net worth.Minimize Lifestyle Inflation

As income grows, resist the urge to spend more on luxury items. Redirect extra earnings toward investments, debt repayment, or savings.Reassess Assets Regularly

Evaluate investments, property, and high-value items periodically. Sell underperforming assets or things that don’t contribute to long-term wealth.Protect Your Assets

Insurance, health, life, property, or liability prevents financial setbacks that can erase years of savings. Unexpected events like medical emergencies or accidents can significantly reduce net worth without protection.

Common Mistakes in Calculating Net Worth

Even seasoned individuals can miscalculate their net worth if they overlook key factors. Avoid these pitfalls:

Ignoring Liabilities: Small debts, unpaid bills, or overlooked loans can inflate your net worth.

Overestimating Assets: Using original purchase prices instead of market value can mislead your financial planning.

Not Accounting for Depreciation: Cars, electronics, or collectibles lose value over time. Include realistic depreciation.

Forgetting Retirement Accounts: Even if funds aren’t immediately accessible, retirement accounts are part of your long-term net worth.

Net Worth Across Life Stages

Your net worth naturally changes over your lifetime, and knowing typical patterns can help set realistic expectations:

Young Professionals (20s-30s)

Often start with negative net worth due to student loans or early investments. Focus should be on debt reduction, building an emergency fund, and starting small investments.Mid-Career (30s-50s)

Net worth grows with career progression, property acquisition, and investment accumulation. Strategic planning and disciplined saving become key drivers of wealth growth.Pre-Retirement (50s-60s)

Focus shifts to wealth preservation, optimizing retirement accounts, and managing risk. High-value assets like property and retirement funds dominate.Retirement (60+)

Net worth may decline as funds are drawn to support living expenses. Planning for sustainability is critical to maintain quality of life.

Using Net Worth to Make Financial Decisions

Your net worth isn’t just a number, it’s a practical tool for everyday and long-term financial decisions:

Buying a Home: Helps determine affordability and down payment capability.

Investing: Shows how much risk you can safely take.

Career Choices: Provides insight into whether you can afford to take entrepreneurial risks or pursue new opportunities.

Retirement Planning: Ensures assets align with your desired retirement lifestyle.

Tools to Track Net Worth

Tracking net worth manually can be tedious, but technology makes it simple:

Spreadsheets: Google Sheets or Excel allow detailed tracking and full customization.

Personal Finance Apps: Mint, YNAB, Personal Capital, or similar apps can automatically sync accounts and provide real-time updates.

Financial Advisors: Professionals can create detailed net worth statements and projections, helping with investment and retirement planning.

Psychological Benefits of Knowing Your Net Worth

Beyond the math, understanding your net worth provides peace of mind and empowers decision-making:

Reduces financial anxiety by making money matters transparent.

Encourages proactive financial behavior rather than reactive spending.

Builds confidence, knowing exactly where you stand and what steps to take next.

By tracking and improving your net worth, you gain control over your financial future, not just for today, but for decades to come.

Conclusion

Your net worth is far more than just a number on a spreadsheet, it is a mirror of your financial health and a roadmap that can guide every decision you make about money. It reflects your habits, priorities, and long-term planning, showing both where you stand today and the potential for tomorrow. By calculating it accurately, you gain clarity and insight that income statements or bank balances alone cannot provide.

Understanding your net worth empowers you to make smarter financial choices. Whether your focus is paying down debt, growing investments, buying a home, or planning for retirement, knowing your net worth gives you a clear picture of what’s possible and where to direct your efforts. It turns abstract financial goals into measurable targets and provides a tangible way to track progress over time.

The key is to start now, take the time to list your assets, tally your liabilities, and calculate the difference. Review this number regularly, make strategic adjustments, and celebrate even small improvements. Every step you take, paying off a loan, contributing to an investment account, or simply saving more builds momentum and compounds into long-term financial strength.

Your net worth is not just a reflection of what you have, it’s a tool that, when used wisely, can guide you toward financial freedom, peace of mind, and confidence in your future. Treat it as a living measure of your progress, track it diligently, and let it inform the decisions that will shape the life you want to create.

Start today. Know your number. And use it to build a future where your financial goals are not just dreams, they are realities.

Interesting Reads:

- 10 Smart Ways to Track Expenses Without Feeling Restricted and Still Enjoy Life

- 21 Personal Finance Basics Every Adult Should Know for Financial Freedom

- How Inflation Affects Your Savings and What to Do: 9 Brutal Truths You Must Know

- 17 Brutal Common Budgeting Mistakes Keeping People Broke in 2026

- How Much Cash Should You Keep vs Invest: 7 Smart Strategies for Financial Security

- Top 25 Best High‑Yield Savings Accounts in the US, UK & Canada

- Personal Finance Guide for Building Wealth in 2026: 18 Proven Strategies That Work